Racial Equity Commission helps kill association health plans

By Marc E. Fitch,

7 hours ago

“I can never take this bill out again,” said a frustrated Rep. Kerry Wood, D-Rocky Hill, of the latest attempt to allow businesses and nonprofits to purchase health insurance through an association (AHP) or form self-funded multiple employer welfare arrangements (MEWAs) for the purposes of healthcare.

“It caused my colleagues a lot of pressure, unnecessarily, from these groups. It’s too controversial in the Capitol but if you talk to any random small business owner or nonprofit, they are desperate for this,” Wood said, who has struggled in vain the past two years to pass this bill that Connecticut businesses and nonprofits say will help them lower their insurance costs.

Those “groups” largely come from under the Capitol dome, and, according to sources, mounted an intense push near the end of the 2024 legislative session to ensure House Bill 5247 never came to pass despite large, bipartisan support and ample support from businesses and nonprofit organizations during public hearing.

The Insurance and Real Estate Committee, of which Wood is co-chair, failed to vote on any legislation before their deadline this year following a breakdown in communication and disagreements over bills. Lawmakers on the committee scrambled to find other legislative vehicles through which to pass some of those bills – and the AHP/MEWA bill was one of those pieces of legislation lawmakers like Wood hoped to get through.

The rising cost of health insurance has been a source of frustration for the public, including small businesses, and for lawmakers who issue public statements every time an insurance company submits a request for a rate increase but have found little agreement on how to move forward with legislation. The AHP/MEWA bill was seen — not as a solution — but as an alternative to the traditional insurance market, particularly the small group market that has been shrinking as more and more insurers withdraw from offering plans.

“I was promoting MEWAs for the last three years because I have gotten nothing but support from the business and nonprofit community to help them lower their costs,” Wood said. “So, we came up with a solution with everybody at the table – Department of Insurance, Office of the Healthcare Advocate, Senate Democrats, Senate Republicans, all of us worked on this together. We found a solution and then we have all of these entities fighting us and they’re not representative of what the public wants.”

“Before the session, most of us do town halls, and we had meetings with our chambers of commerce and one on ones with constituents and this was honestly the biggest issue I heard about that people wanted. It’s frustrating because it seems like the only people who don’t want it are the people in the Capitol,” said Rep. Raghib Allie-Brennan, D-Bethel, who was a co-sponsor of the bill. “Obviously, the rising cost of healthcare is a concern for everyone, not just small businesses, but we have an opportunity here to make sure they can lower costs.”

Wood has certainly faced opposition in the past in her push for this bill, particularly from members of her own party and from state agencies paid for with taxpayer dollars.

Last year, Sen. Matthew Lesser, D-Middletown, attempted to filibuster the bill during an Insurance and Real Estate Committee meeting; then Access Health CT – the state’s healthcare exchange – made a last-minute move to torpedo the legislation , primarily because they receive fees on the sale of small group insurance in Connecticut and allowing small businesses to go elsewhere would affect their bottom line.

This year, opposition came from many of the same groups who have opposed the legislation in the past, according to emails, interviews, and public hearing testimony: state employee unions who enjoy some of the best, low-cost insurance in the country; teacher unions who also enjoy great benefits; the organization Husky 4 Immigrants, who are pushing for taxpayers to cover healthcare costs for undocumented immigrants, and a bevy of medical associations like the Leukemia and Lymphoma Society.

Access Health CT, the state’s insurance exchange, also mounted an effort to ensure the legislation didn’t pass this year, according to Rep. Tom Delnicki, R-South Windsor.

“They had been in communication, I believe, with just about every legislator that would be involved with that and pleading their case,” Delnicki said. “Let’s face it, Access Health CT has got a dog in the fight, they’re trying to be competitive, but I’m sure that people would have saved money going with the MEWA or going with the association plan.”

There was also opposition from the Office of the Healthcare Advocate, despite the office working with lawmakers on crafting the bill. This was also not particularly new, the office having opposed the bill in the past over concerns that it “could potentially undermine the success of the [Affordable Care Act].”

But this year, much of the opposition came from people and organizations connected to the Commission on Racial Equity in Public Health, a commission created in 2021 through an amendment to Senate Bill 1 , a massive mental health bill focused on youth during the pandemic. The commission is charged with understanding and reporting on structural racism in health care and developing a plan to eliminate “health disparities and inequities,” and costs about $555,000 in taxpayer dollars, according to the fiscal note.

The Commission is chaired by Ayesha Clarke, who was appointed by House Speaker Matthew Ritter, D-Hartford, and who also serves as the executive director of Health Equity Solutions, a nonprofit organization focused on eliminating racial disparities in Connecticut’s health care system. Clarke replaced the previous chair, Tekisha Dwan Everette, who was also executive director of HES at the time. In her role on the Commission, Clarke also works with Access Health CT’s Director of Health Equity Tammy Hendricks.

While the Commission initially counted 22 members, the number has dwindled, according to their latest bi-annual report to the legislature in January of 2024, which indicated that legislative changes altered appointments to the Commission, and there were a number of vacancies. Meeting minutes on the website are sparse and appear dysfunctional at times. The Commission’s website only shows one meeting in June of 2024, and the meeting minutes are from February of 2023. There is also an advertisement for a symposium on Cementing Equity in State Government. One has to go back to April of 2023 to find readable minutes.

Representatives of the Commission and lobbyists for HES essentially argue that allowing association health plans and MEWAs for businesses would exacerbate racial inequalities in health care, and basically double down on institutional racism.

“Because people of color are disproportionately impacted by chronic disease, businesses who employ a greater number of Black and Brown people will likely be charged more than businesses with a great number of White employees,” Gretchen Shurgarts, analyst for the Commission on Racial Equity in Public Health wrote in public hearing testimony. “The commission is concerned that due to inequities in current health outcomes, the higher costs born will likely fall along racial lines.”

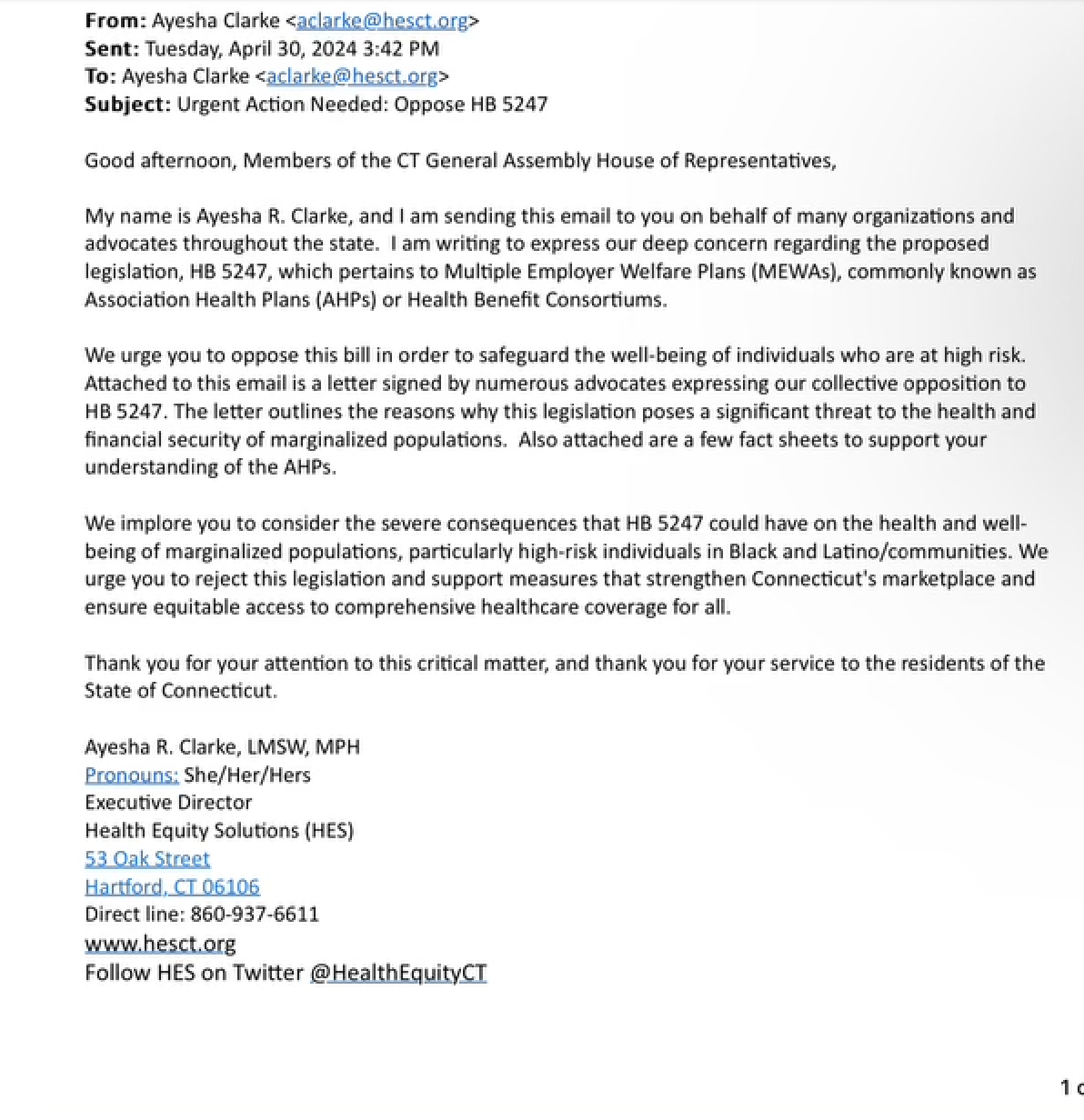

But as the legislative session began to draw to a close in late April, Clarke sent emails to lawmakers warning them off attempts to pass the bill through another legislative vehicle.

Clarke sent an April 20, 2024, email , signed by numerous other organizations, to lawmakers imploring them to reject the legislation and claiming it would have “severe consequences” for “marginalized populations.”

{kind=link}

“We urge you to oppose the bill in order to safeguard the well-being of individuals who are at high risk,” Clarke wrote. “We implore you to consider the severe consequences that HB 5247 could have on the health and well-being of marginalized populations, particularly high-risk individuals in Black and Latino/communities. We urge you to reject this legislation and support measures that strengthen Connecticut’s marketplace and ensure more equitable access to comprehensive healthcare coverage for all.”

“Should AHPs/MEWAs/Health Benefit Consortiums arise as an amendment this year, the undersigned groups will work to use any legislative options available to prevent them from being offered in Connecticut,” said a follow-up April 29 email signed by numerous organizations with HES at the top.

But it wasn’t just strongly worded emails. Clarke’s organization actively and intensely lobbied lawmakers, distributing fact sheets compiled by HES that claimed AHPs and MEWAs are not insurance , will charge more to businesses based on pre-existing conditions thereby discriminating against pre-existing conditions, will have limited state oversight, and that businesses are in dangers of having to pay for medical claims if the AHP or MEWA goes bankrupt, all with the insinuation that the plans will hurt the cause for racial equity.

“AHPs are discriminatory against people of color, women, people with disabilities, and older adults,” said another fact sheet distributed by HES . “Because people of color, women, people with disabilities, and older people disproportionately suffer from higher rates of chronic diseases or expensive conditions (such as pregnancy), a policy that uses health status to set rates is inherently discriminatory toward these groups.”

“I’m a member of the Black and Puerto Rican caucus and I do take into account comments that these policies could be racist. What we’re talking about here is a legal structure which in itself is not discriminatory,” Allie-Brennan said. “I think sometimes people try to use unfair arguments. I’m a person of color, I do take it seriously, accusations that we’re supporting legislation that might be discriminatory. My response is to show us how that is. Obviously, 43 other states are implementing this, why can’t we focus on making it better?”

“It’s one thing to lobby against something, it’s another thing to brand it in terms that, quite honestly, aren’t appropriate,” Delnicki said. “There was some lobbying that, quite frankly, didn’t comport with what the reality of the plans are.”

Health Equity Solutions (HES) was formed in 2014 with a stated goal to dismantle systemic and institutional racism in health and, according to their tax filings, has grown rapidly over the last ten years, particularly in the last five years during the COVID-19 pandemic.

Since 2019 the organization has received $1.1 million in funds through the state for advertising and management consultation services, according to the state’s open data portal. Most of that — $697,000 – came from federal COVID-relief dollars.

Interestingly, HES also received nearly $88,000 in 2021 and 2022 for management consultant services paid for through the state’s insurance fund , which was established to ensure the Connecticut Insurance Department is funded and is paid for through assessments on insurers. Aside from the federal COVID dollars, the majority of payments were made through the Connecticut Office of Health Strategy.

Those years between 2019 and 2022 also saw HES revenue grow from $734,140 to the $1.4 million listed in their latest tax filing, which is down from the previous years’ $1.9 million.

Lobbyist filings show HES spent $19,000 on lobbying legislators, the CT Department of Public Health, and the Office of the Healthcare Advocate in 2024 with a lobbying firm. The filing also lists three in-house lobbyists including Clarke, and Kally Moquete, who was reportedly distributing the fact sheets to lawmakers to kill the bill with an eye toward racial equity.

According to HES’ State Policy Guide for Health Equity , health runs into nearly all facets of hotly debated topics at the capitol – voting rights, immigration, criminal justice, housing, education, and childcare – all issues reflected in the Commission’s mission to eliminate structural racism.

Among items listed as HES’ policy agenda for 2024 was addressing “social and economic needs through Medicaid,” promoting a “more integrated health system,” ensuring “free health insurance for individuals and families with lower incomes, including immigrants,” and “Work with the Commission on Racial Equity in Public Health to develop and implement a strategic plan for the health equity in CT.”

Reached for comment via email, Clarke said MEWAs and AHPs would “exacerbate health disparities, particularly affecting Black and Latino populations who already face a wealth gap and lower health insurance literacy,” and denied that HES worked with or received guidance from Access Health CT.

According to Clarke, however, there was bad blood on both sides of the lobbying efforts for and against the AHP/MEWA bill, stating she made an executive decision to not meet with Rep. Wood to discuss her concerns with the bill following an encounter between Wood and a member of her team at the Capitol.

“Members of my team did speak with many bill proponents, identified areas of concern with the bill language and discussed potential alternatives to mitigate the disproportionate impact on small businesses that employ women, individuals with disabilities, the elderly and those with preexisting health conditions,” Clarke said. “During an encounter with a legislator, while discussing this, Representative Wood entered the conversation and created a hostile environment for one of the members of my team and began calling her names.”

“This occurred on two separate occasions in the presence of others,” Clarke continued. “As a result, I made the executive decision to refrain from scheduling an in-person meeting with her. However, my team continued to meet with many bill co-sponsors.”

Rep. Wood denies insulting, or creating a hostile environment for anyone. Rather, she says, she was trying to have a “constructive debate” on the issues.

“My intention was to confront the opponents of the legislation and have a constructive debate on how best to move it forward,” Wood said. “We had over three dozen sponsors and growing, yet misinformation and inaccuracies kept being passed around the building.”

Clarke said that instead of the MEWA bill, they supported HB 5054, An Act Addressing Health Care Affordability as “a better alternative,” saying the legislation “aims to address heathcare affordability, particularly high prescription drug prices that disproportionately impact racial minorities.”

HB 5054 was the governor’s bill and would have created an oversight board for prescription drug affordability and a commission on cost growth benchmarks under the Office of Health Strategy (OHS).

That bill, however, was pulled by OHS, wanting more time to work on it, but HES lodged several other legislative wins for their cause, including expanding Connecticut’s paid sick leave law, which passed over the protestations of businesses and Republicans, and prohibiting medical debt from affecting credit scores, both of which were signed by Gov. Ned Lamont. Preventing medical debt from being included on credit scores is now being considered at the federal level.

Reached for comment, Healthcare Advocate Sean King confirmed his office had worked on the legislation with Wood and other proponents in 2023, but felt that there was some language in 2024’s bill that did not offer enough consumer protections.

“We worked pretty closely with the Insurance Committee, the [CT Insurance Department], industry, and other folks on trying to make sure a bill was crafted that was going to pass would contain enough consumer protections in it that we felt that it would not be harmful to consumers,” King said. “The version of the bill last year had gotten to the point that our office — I wouldn’t say supportive — but we thought it was adequate.”

“This year’s version of the bill was a little bit different. I think the intent was there, but our problem was we felt the language had changed just enough to the point where, again, the CBIA and other people who participated in crafting the bill this year had the intent of maintaining the same consumer protections discussed in last year’s bill, but we felt the language maybe didn’t capture that, so if a bad actor wanted to enter that space, they could take advantage of some ambiguities in the bill.”

But those were not the only issues the Commission was lobbying for or against during the session, and the other insurance-related issue could leave Connecticut businesses in a tricky situation.

Not long after the end of the legislative session, one of Connecticut’s major insurance companies, Aetna, announced it would be leaving the small group health market. While Aetna didn’t account for much of the small group market, Cigna, which had supplied a large number of small group plans, had just exited as well. Aetna was the fourth insurer to abandon small group, leaving only two companies offering those plans in Connecticut.

The small group market has been shrinking as rising insurance costs have pushed small businesses to what are called level-funded plans, basically a self-insured healthcare plan for small groups backed up with stop-loss insurance. Stop loss insurance is essentially catastrophic insurance. For a small business owner who is self-funding health care, one or two major claims – cancer for instance – could bankrupt them quickly, so they purchase additional insurance from a company.

More and more, small businesses have been turning to level-funded plans. According to the Kaiser Family Foundation, level-funded plans covering employers with fewer than 200 employees accounted for 6 percent of the market in 2018. By 2023, it was 38 percent. In Connecticut, that number has gone from 3 percent to 24.4 percent, according to Ellen Andrews , citing data from the Connecticut Insurance Department.

Level-funded plans are largely out from under the regulatory burdens Connecticut places on small group insurance – the only form of insurance the state has any real say over — and are instead regulated by the federal ERISA guidelines. Businesses see them as more flexible with the ability to offer cost-savings, but those plans have also drawn the ire of the Commission on Racial Equity in Public Health and HES.

“We advocate for regulating or restricting the use of stop-loss/level-funded insurance products, which we believe hurt consumers,” Clarke said. “We emphasize the importance of comprehensive and regulated healthcare to ensure affordability and coverage for small employers and employees.”

Another fact sheet authored by the commission’s executive director Pareesa Charmchi-Goodwin, however, argued that level-funded plans remove healthy people from Access Health CT, driving up costs for those who remain; are risky junk plans that leave people in danger of medical debt; and that level funded plans do not conform with the Affordable Care Act.

“CT should join NY in protecting our small businesses by passing legislation preventing insurance companies from selling to employers with fewer than 50 employees,” the fact sheet concluded.

Basically, it could be a catch-22 for small businesses: On the one hand, they’re being actively prevented from pooling together resources to either purchase insurance or self-fund health coverage, while simultaneously facing the threat that their level-funded plans could be removed – two positions being pushed by the Commission on Racial Equity in Public Health and HES.

“They are problematic from a health equity perspective because they effectively assign a participation price by health risk of the employment pool of small groups while providing insufficient assurances to the quality of the product,” Charmchi-Goodwin said. “That means if an employer has a population of employees with pre-existing conditions their cost will skyrocket.”

“Proposals like the 2024 AHP/MEWA bill further deteriorate the fully insured market, increasing plan costs,” Charmchi-Goodwin continued. “As far as health insurance policy design – market segmentation is the biggest driver of fully insured plan cost increases.”

The argument over market segmentation – the siphoning away of people in the fully insured market – is a chicken or egg issue. The Affordable Care Act changed the insurance industry nationwide, many would argue for the better, but it did come at a cost, and as those costs began to rise businesses began looking for alternatives to the fully insured market. As people and businesses leave the fully insured market, there are fewer people to pool together to contain costs, and insurance rates go up again.

Charmchi-Goodwin says Connecticut should strengthen the fully insured market by decreasing segmentation, which would therefore increase affordability.

Healthcare Advocate Sean King also believes that stop-loss insurance for small, self-insured plans need to be reined in, because he says major health claims in those small groups can bankrupt them or cause the stop loss insurance to not be renewed.

“The thing we would prefer, and would like to address, is the proliferation of self-insured plans penetrating more and more into the small group space. Those plans, using stop loss, are able to bypass all of the state mandates and consumer protections the state of Connecticut has passed,” King said. “It’s a temporary solution for many small businesses because as soon as somebody has a health issue, it can be hard for them to renew.”

However, King also concedes that AHPs and MEWAs could provide better protections for small businesses, assuming the enabling bill has the consumer and price protections his office sought in the language. “That was part of the hope and intent was to draw people away from the stop-loss market into a market that is more protective of employees,” King said.

Jeffrey Hogan of Upside Health Advisors in Farmington, who manages “hundreds” of level-funded plans and testified in support of the AHP/MEWA bill says that argument is “on its face, inaccurate.”

“The market itself, and market results, have proven that employers have chosen level-funded plans as their preferred employer sponsored group plan platforms for a variety of reasons,” Hogan said, adding the plans give employers greater flexibility, performance data, and cost savings with the employer and employees receiving money back if the plan performs better than expected, and leveling out the increases in bad performing years.

“Really, what’s happened in the Connecticut marketplace, and other marketplaces that were predominantly for middle market and small group employers fully insured plan markets, it significantly reduced the cost of care,” Hogan said. “It’s given them more and better plan design that is most appropriate to the needs of that specific group.”

“The robust fully insured marketplace has virtually been eclipsed by level funded plans because employers and plan beneficiaries prefer these plans,” Hogan continued. “Basically, every carrier in this marketplace took market cues. They all have very competitive level-funded offerings in the marketplace and the assertion that it is discriminatory, that the underwriting is discriminatory, is just patently wrong.”

“Self-insured level funded plans serve a critical need for affordable health care coverage in Connecticut’s small group market,” said Susan Halpin, executive director of the Connecticut Association for Health Plans. “The number of employers migrating to these products clearly demonstrates the demand. One can only imagine the outcry from small businesses if the legislature acts to restrict these plans as lobbied for by several advocacy organizations.”

But while level-funded plans and AHPs/MEWAs could contribute to segmentation, the state of Connecticut has already contributed amply to that segmentation. The state’s employee health plan is, for one, a self-funded plan.

Secondly, the state opened its health plan to municipal employees under its Partnership Plan 2.0 – essentially siphoning off 156,000 people from the fully insured market. Expanding Medicaid enrollment could also be seen as another form of segmentation by covering more people under the government program.

“Insurance is an ecosystem – if you introduce a product that is designed to siphon ‘healthy’ groups from a community-rated pool, the community-rated pool will become more ‘risky’ and therefore more expensive,” Charmchi-Goodwin said. “These plans offer a false solution that will only compound the problem; not solve them.”

“You could make the argument that these plans have killed the fully insured marketplace: it has,” Hogan said. “Because those plans weren’t as beneficial to the employers and employees, nor did it share savings back to the employees the way these level-funded plans do. It’s just how marketplaces work.”

Many of the same groups opposed to AHPs and MEWAs for businesses, including HES, have advocated in the past for the ultimate segmentation – legislation pushed by former Comptroller Kevin Lembo called the public option – and Rep. Allie-Brennan believes that much of the opposition to HB 5247 stems from the often-heated battle over the public option that took place in 2018, 2019, and 2021.

“That fact that you have a bipartisan group that wants this done and it’s not getting passed, I think to myself, what is the issue here?” Allie-Brennan said. “I think it’s from people wanting the public option. They think this goes against that.”

“Some of these groups, by the way, are the same organizations that are pushing hard for a government-run health care system which makes one question if their efforts against level-funded plans are just part of that broader agenda,” Halpin said.

The public option healthcare proposal was put forward several times as legislation with the full backing of high-ranking Democrats, the popular comptroller, and the same groups fighting to eliminate the AHP/MEWA bill, but the proposal never made it past the finish line.

Essentially, the legislation would have allowed the comptroller’s office to open the state employee health plan to small businesses and, conceivably, individuals through the state’s Partnership Plan 2.0, which allows municipalities to do the same, but has faced some funding concerns in the past, as well as concerns for taxpayers footing the bill if claims outpaced premiums.

The proposed legislation was opposed strongly by Connecticut’s insurance industry, citing, among other things, the fact that the public option would double down on the Partnership Plan 2.0 which the industry argued was already killing the market.

“The Comptroller’s program has undermined the private market by intentionally underpricing coverage,” Halpin wrote in testimon y at the time. “Plans in the private market, which are subject to state taxes and assessments as well as regulatory requirements that include guaranteed issue, rate review and approval, small group rate methodology, a medical loss ratio, and solvency standards among others, that the Comptroller is completely unburdened by, are put at an unfair competitive disadvantage. These private carriers can’t compete with a program that gets to use state taxpayer dollars to cover built-in shortfalls.”

Essentially, the Partnership Plan 2.0 allowed municipalities to form a pool under the state’s self-funded health plan that, since it wasn’t subject to all the taxes, fees, and regulations of the state like private insurers, was able to offer a lower cost product, siphoning the insurance industry’s customers and, if the argument is correct, potentially driving up costs in the fully insured market.

During debate over the public option in 2021 during an Insurance and Real Estate Committee meeting, Rep. Wood proposed an amendment to the bill that would require the public option to be treated like insurance companies, which would have effectively gutted the savings envisioned by Lembo. Her amendment was passed over the protestations of Sen. Lesser, her co-chair, who two years later would mount his filibuster against the AHP/MEWA bill.

There was plenty of support for the public option among some powerful lobbying groups, and, interestingly, among the same nonprofit group that supported the MEWAs, suggesting they’d be happy with anything that would help lower their costs. But there was also ample opposition from the Connecticut Business and Industry Association (CBIA) and Republicans. Gov. Ned Lamont waffled on the issue several times, before finally withdrawing suppor t.

Comptroller Lembo then resigned from his position at the end of 2021 due to health concerns, Sean Scanlon was voted into office, and Lesser is no longer co-chair of the Insurance and Real Estate Committee; there may be some lingering hard feelings under the Capitol dome.

“I think that some people don’t think that this can exist next to a public option, and I think they’re wrong,” Allie-Brennan said. “I think that is what is at the root of this, that people want the public option and nothing else, and I think that’s where you see this stemming from.”

Rep. Delnicki says the first industry to approach the Insurance and Real Estate Committee regarding association health plans and MEWAs was the Connecticut Brewers Guild around 2017.

“I’m not sure how many folks the brewers actually employ, but the point being, you take that, multiply it 169 towns and you’ve got a lot of folks, and they could easily form an employee welfare association,” Delnicki said. “They were one of the first people that came to us wanting to have legislation passed to allow them to have the same thing cities and towns have been able to do.”

For all the claims that association health plans or MEWAs would hurt the people they are supposed to protect, Connecticut allows municipalities and boards of education to join together for purchasing healthcare insurance, basically association health plans, under legislation passed in 2010.

According to House Bill 5424 , signed into law fourteen years ago, “two or more municipalities or local or regional boards of education, or any combination of these, to enter into a written agreement to act as a single entity to provide employee medical or health care benefits under certain conditions.” The legislation was supported by a large bipartisan group of lawmakers and passed unanimously in the House and Senate. It was also “strongly” supported by the teacher unions, as well as Connecticut’s municipal associations and the Hartford Public Schools superintendent.

“The Connecticut Education Association has been a strong proponent of reducing healthcare costs by creating larger ‘pools’ of members,” CEA Director of Government Affairs said in written testimony. “The simple reality is that the biggest cost drivers of Board of Education budgets are healthcare costs and any method to reduce these costs should be explored.”

The American Federation of Teachers (AFT) – which testified against allowing association health plans for businesses – also supported the bill “conceptually.” Based on the bill’s history, it was hardly controversial in 2010.

“This is nothing new,” Delnicki said. “I can remember being on the town council when the town manager brought this forward. We did it and, I’ll be blunt, we had a catastrophic healthcare policy that we bought. We put out an RFP for somebody to administer the program, we actually took money out of the fund balance and put it into the plan. About 900 or so folks constituted the plan and it’s been in operation now for quite some time now.”

Delnicki admits that it isn’t technically insurance – one of the points of criticism by opponents of the AHP/MEWAs — “but technically, it does the same thing.”

He said the plan is self-funded, backed up with stop loss insurance that has come in handy when they’ve had major health events among South Windsor employees. It was also something the town had to bargain for with its municipal unions, meaning that the plan had to live up to the requirements of the collective bargaining contracts.

South Windsor is not the only town that uses the legislation passed in 2010 for health insurance. Plainfield, Coventry, Putnam, and Tolland all joined together to form the Eastern Connecticut Health Insurance Program (ECHIP) under the same enabling legislation, and now covers 1,523 employees and 4,500 members, according to its website.

Lisa Thomas, chair of the Coventry Town Council, said the collaborative has saved the town “tons and tons” of money since its inception.

“We did it along with our board of education, and we did it for two reasons,” Thomas said. “It gave us more predictability when it came to be budget time, and it gave us better control over expenses, and it’s saved us tens of thousands of dollars.”

“I know our costs went up more than usual the past two years because we had some higher experience, prior claims, but we have felt that it was a great decision and has continued to be,” Thomas continued.

The towns of North Haven, Ansonia, and East Haven joined together in 2017 under the ACES Health Insurance Collaborative Services Group . In 2018, they announced healthcare savings for members of $3.4 million . According to meeting minutes, the collaborative also utilizes stop-loss insurance and has been facing higher-cost claims lately, increasing the cost of stop-loss by roughly 2 percent.

“Look at any of the cities or towns that that are doing this, they’ve got virtually every demographic working in the community and no one’s discriminated against,” Delnicki said.

The fact that Connecticut allows this for governments but not for businesses has been one of the arguments used by proponents of the bill to support passage.

“HB 5427, if enacted, will finally provide a platform for these small employers to take advantage of the self-funded arrangements that larger employers, the state, municipalities, and unions take advantage of today,” wrote CBIA Assistant Counsel Wyatt Bosworth in public hearing testimony

Now, however, passage of such a bill for businesses has become politically tinged from the top down, with claims that AHPs and MEWAs for businesses in Connecticut are “Trump era health insurance,” according to Delnicki and others.

“There were a number of folks that were calling it Trump era health insurance, which it wasn’t,” Delnicki said. “We’ve had these plans in before Donald Trump ever realized or ever thought about running for president.”

Naturally, it wasn’t just one side lobbying the AHP/MEWA bill in the last days of session. The CBIA sent out their own fact sheets disputing those put out by HES, and an email to lawmakers with an equally long list of backers ranging from chambers of commerce and business associations to the CT Nonprofit Alliance, as well as individual businesses, imploring legislators to push it through.

“The concept behind this legislation is simple – it allows trade associations to provide healthcare benefits for member employers,” CBIA President Chris DiPentima wrote in an April 24 email . “Pooled together, small employers will have the ability to purchase insurance or provide self-funded health plans in much the same way that large employers, municipalities, and union trusts do, using the power of numbers to achieve savings that aren’t otherwise possible.”

“HB 5247, in contradiction to recent letters sent by opponents of the bill, also prohibits discrimination against individuals with pre-existing conditions and discriminatory and actuarially unsound rating methodologies,” DiPentima continued. “It is illegal under federal law, and codified under the bill, to discriminate against individuals based on health.”

But it wasn’t enough in a short session that saw no vote by the Insurance and Real Estate Committee and a flurry of intense, racially charged opposition, and whether the legislation will be brought up again is now in doubt.

CBIA President Chris DiPentima expressed disappointment in the failure of the bill in a CBIA blog post following the end of session.

“For the second consecutive session, lawmakers were presented with bipartisan, transformational legislation that would change the lives of hundreds of thousands of small business employees,” DiPentima said. “There was a meaningful solution on the table, and it is incredibly frustrating that the bill failed to even receive a committee vote.”

About a month after the end of session and the failure of the AHP/MEWA bill, Connecticut insurers submitted rate increase requests to the Connecticut Insurance Department, including an increase to small group plans that are not on Connecticut’s insurance exchange of average rates between 5 and 9 percent.

“There was some pretty aggressive lobbying that killed [HB 5247],” Delnicki said. “It’s sad that it never got a fair hearing, it’s sad that it never had a chance to come out of the Insurance and Real Estate Committee and even go through one chamber of the legislature, so at least there could be some kind of a fair debate or a fair discussion as to what it can and what it can’t do. That would have been very healthy. I know there’s going to be nonprofits that are going to looking again next year, I know that the business community is going to be looking for it next year.”

“It was very heated,” Allie-Brennan said. “I just think that Rep. Kerry wood, the chair of the committee, has been unfairly demonized throughout this whole process. She really just wants to offer a better solution for thousands of people across the state.”

The post Racial Equity Commission helps kill association health plans appeared first on Connecticut Inside Investigator .

Most Popular

Most PopularWelcome to NewsBreak, an open platform where diverse perspectives converge. Most of our content comes from established publications and journalists, as well as from our extensive network of tens of thousands of creators who contribute to our platform. We empower individuals to share insightful viewpoints through short posts and comments. It’s essential to note our commitment to transparency: our Terms of Use acknowledge that our services may not always be error-free, and our Community Standards emphasize our discretion in enforcing policies. We strive to foster a dynamic environment for free expression and robust discourse through safety guardrails of human and AI moderation. Join us in shaping the news narrative together.

Comments / 0